TL;DR:

- Malta’s office market requires strategic decisions for leasing, fit-out, and operations to optimize costs.

- Understanding total occupancy costs and local market nuances improves tenant outcomes and negotiations.

- Sector-specific demand, location knowledge, and experienced local advice are key to success in Malta’s market.

Malta’s commercial office market is more nuanced than many international businesses expect. While the island’s reputation for competitive rents and a thriving iGaming and fintech ecosystem is well established, the actual process of leasing, fitting out, and operating office space involves strategic decisions that significantly affect both cost and business outcomes. In this case study rental office in Malta scenarios, real case studies from Sliema, SmartCity, and Mriehel reveal that informed tenants consistently achieve better terms, lower occupancy costs, and more suitable spaces than those who rely on surface-level market knowledge.

Table of Contents

- Malta’s evolving office rental landscape

- Cost benchmarks and space requirements: data from real case studies

- Fit-out responsibilities and lease structures: lessons from recent deals

- Keys to a successful office rental: what case studies reveal

- Why learning from local case studies outperforms generic advice

- Need help finding the right Malta office? See your options

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Malta’s competitive rental market | Office rents are significantly lower than Western Europe, especially in prime areas like Mriehel and Sliema. |

| Fit-out costs matter | Tenants usually bear fit-out responsibilities, making it vital to factor these into your budget. |

| Success relies on case-driven insights | Learning from real Malta office case studies yields practical strategies for better leasing decisions. |

| Key sectors drive demand | iGaming, fintech, and financial services continue to anchor Malta’s office rental growth. |

| Local expertise is invaluable | Relying on regional knowledge and past case studies improves outcomes when renting office space in Malta. |

Malta’s evolving office rental landscape

Malta’s office market has matured considerably over the past decade. Demand is now concentrated in specific high-value sectors: iGaming, fintech, financial services, aviation, and international SMEs seeking EU-based operations. This demand has pushed prime locations including Sliema, St Julian’s, and the Mriehel business district into the spotlight, with each area offering a distinct profile of costs, tenant mix, and infrastructure quality.

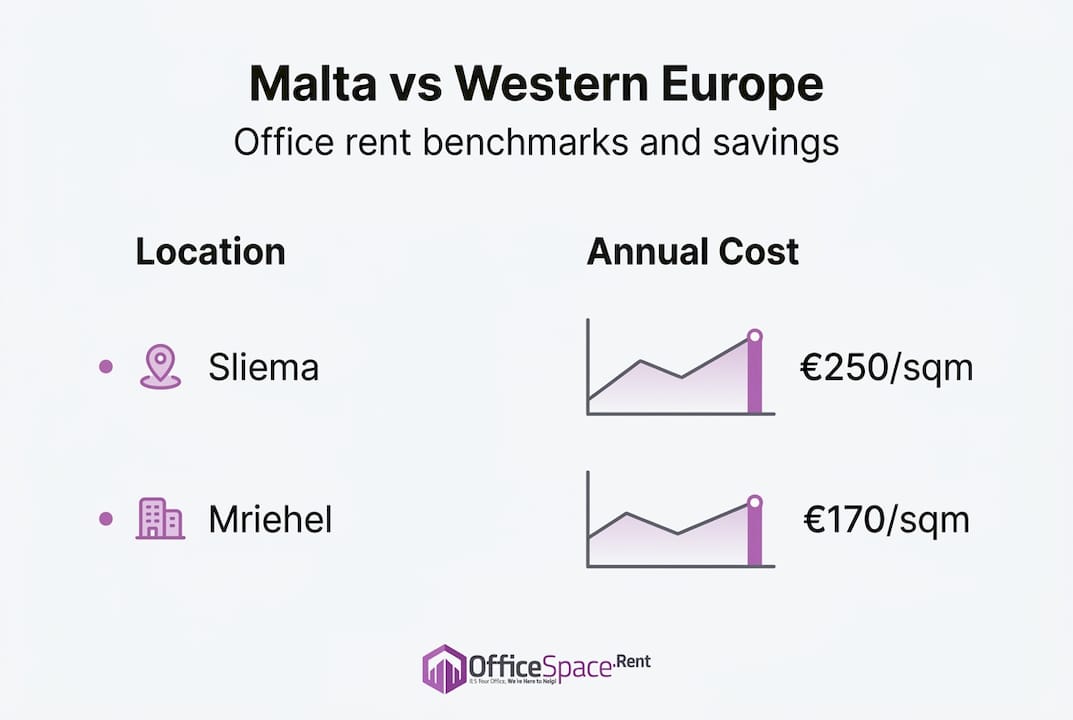

Prime office rents in Sliema and St Julian’s range from €270 to €380 per square metre per year for seafront or prominently positioned buildings, while the Mriehel Central Business District typically averages €170 to €250 per square metre per year. These figures reflect a market that rewards location knowledge and early engagement with available stock.

What makes Malta stand out from its EU peers is a combination of structural advantages. English fluency, EU passporting, a concentrated iGaming and fintech ecosystem, flexible lease terms, and rents that remain substantially lower than Western European capitals all contribute to sustained international interest. For businesses scaling in Europe, these are material operational advantages, not just marketing points.

Key factors influencing location choice in Malta include:

- Proximity to talent pools: St Julian’s and Sliema attract multilingual professionals, particularly important for iGaming and customer operations.

- Transport and connectivity: Mriehel offers easier car access and larger floor plates, making it popular for back-office and technology functions.

- Business ecosystem density: Clusters of sector-specific service providers, law firms, and accountants in prime areas reduce operational friction for new entrants.

- Flexibility of lease terms: Shorter initial terms with renewal options are more commonly available in Mriehel than in central Sliema.

“Malta’s combination of English-language proficiency, lower operating costs, and EU regulatory access creates a compelling proposition for international firms establishing European headquarters or regional hubs.”

Pro Tip: Before committing to a district, map your talent recruitment strategy. St Julian’s workspaces attract a different workforce profile than suburban business parks, and this matters for hiring speed and staff retention. Sector hotspots also shift over time, so consulting current vacancy data is worth the effort.

Cost benchmarks and space requirements: data from real case studies

Understanding what office space in Malta actually costs requires moving beyond headline figures. Tenants who have successfully negotiated leases in the market consistently point to the gap between advertised rates and the true total occupancy cost, which includes service charges, fit-out amortisation, and utilities.

The table below illustrates how Malta’s key office districts compare on a practical cost basis:

| Location | Avg rent (€/sqm/yr) | 300 sqm annual cost | Equivalent Dublin cost |

|---|---|---|---|

| Sliema (prime) | €250 | €75,000 | €180,000+ |

| Mriehel CBD | €170 | €54,000 | €180,000+ |

| St Julian’s (seafront) | €320 | €96,000 | €180,000+ |

These figures make a strong case for Malta relative to Western European alternatives. A 300 sqm office in Mriehel costs approximately €54,000 per year, compared to roughly €180,000 for equivalent space in Dublin. That differential can directly fund additional headcount or technology investment.

📊 Key statistic: Tagliaferro Business Centre in Sliema accommodates 7,000 sqm of office space across multiple floors, housing approximately 650 staff with iGaming as its anchor sector. The building achieved near-full occupancy after a full refurbishment, illustrating strong demand for quality, refitted stock in central Sliema.

The Tagliaferro case is instructive because it demonstrates how refitted Grade A space attracts tenants from iGaming, aircraft leasing, IT, and financial services simultaneously. Multi-sector buildings like this create an ecosystem effect, where proximity to complementary businesses adds operational value beyond the physical space.

For businesses assessing their space requirements, space planning for SMEs is often underestimated. A general benchmark of 8 to 12 sqm per person is widely used in Malta’s market, but technology-intensive teams, compliance-heavy operations, or businesses with regular client visits typically require more. Detailed guidance on workspace sizing should form part of any early-stage planning process.

Pro Tip: Always request a breakdown of service charges alongside the headline rent. In some Sliema buildings, service charges add 15 to 25% to the base rent, materially changing the total cost calculation. This is one of the most common areas where tenants are surprised post-signing. Understanding office investment returns from the landlord’s perspective also helps you negotiate more effectively.

Fit-out responsibilities and lease structures: lessons from recent deals

Cost per square metre is only part of the leasing equation. One of the most consequential decisions in any Malta office deal is determining who bears the cost and responsibility for fit-out works. This is where significant financial exposure can be created, particularly for tenants unfamiliar with local market norms.

The Malta Gaming Authority’s lease at SmartCity provides one of the most documented examples in the local market. The authority signed a 15-year lease at the SmartCity campus and spent €4.3 million on fit-out works, a cost borne by the lessee as is typical in Malta’s market. This figure covers specialist interior works, compliance infrastructure, IT cabling, and security installations appropriate for a regulatory body.

The lesson from this case is that fit-out costs are not marginal. For a purpose-specific operation, fit-out can rival or exceed several years of rent in total value. Fit-out responsibilities can differ between public entities and private sector tenants, and arrangements are sometimes negotiable depending on lease length, covenant strength, and the landlord’s appetite for securing a long-term anchor tenant.

The following comparison sets out how fit-out responsibilities and typical lease structures vary across tenant types in Malta:

| Tenant type | Typical fit-out responsibility | Standard lease term | Fit-out contribution from landlord |

|---|---|---|---|

| Private SME | Tenant | 3 to 5 years | Rare; shell and core only |

| Large corporate | Negotiated | 5 to 10 years | Possible for anchor tenants |

| Public sector | Tenant | 10 to 15 years | Unlikely |

| iGaming operator | Tenant | 3 to 7 years | Occasional fit-out incentives |

Key steps for negotiating fit-out terms and customisations effectively:

- Establish the baseline specification: Confirm whether the space is delivered shell and core, Cat A (basic finishes), or Cat B (ready to occupy), as this directly determines your fit-out budget.

- Request a landlord contribution: For leases of five years or longer, experienced tenants negotiate a landlord contribution or rent-free period to offset fit-out expenditure.

- Appoint a local project manager: Malta has a limited pool of specialist commercial fit-out contractors. Engaging a project manager early secures capacity and controls costs.

- Factor reinstatement obligations: Some leases require tenants to return the space to its original condition on exit. This can be a material cost and should be assessed at heads-of-terms stage.

- Document all agreed specifications: Ambiguity in fit-out schedules is a frequent source of dispute. Ensure all agreed works are annexed to the lease agreement.

For detailed negotiation tips on lease terms and fit-out clauses, reviewing relevant market case studies before entering discussions is strongly recommended.

Keys to a successful office rental: what case studies reveal

Synthesising the evidence from Tagliaferro, SmartCity, and broader market data produces a consistent set of principles that distinguish successful Malta office lettings from costly missteps.

“Businesses that combine English fluency advantages, sector ecosystem positioning, and a rigorous cost model consistently achieve better operational outcomes from their Malta office strategy than those selecting space on price alone.”

The most important steps that emerge from real-world cases include:

- Conduct thorough location due diligence: Assess commute patterns, competitor proximity, talent availability, and transport links before shortlisting buildings.

- Model total occupancy cost, not just rent: Include service charges, fit-out amortisation, utilities, and reinstatement provisions in your financial model.

- Understand lease flexibility before signing: Break clauses, expansion rights, and sub-let provisions are especially important for fast-growing businesses.

- Research landlord reputation: Established landlords with professional management teams reduce operational risk and resolve maintenance issues faster.

- Engage local market expertise early: The Malta office market moves quickly. Buildings in prime locations can go from available to fully let within weeks.

Common mistakes observed across case studies include underestimating fit-out timelines, ignoring service charge escalation clauses, and selecting locations based on price alone without accounting for talent acquisition costs.

Pro Tip: If you expect headcount to grow within 18 months, negotiate expansion rights or an option on adjacent space at the outset. Revisiting terms mid-lease is significantly more expensive and time-consuming. The Malta office space guide provides practical frameworks for modelling growth scenarios within your lease structure.

Why learning from local case studies outperforms generic advice

Generic property advice, even from credible pan-European sources, frequently fails to capture the specific dynamics of a small, fast-moving market like Malta. The island’s office market is shaped by a narrow set of decision-makers, a concentrated geographic footprint, and sector-specific demand that can shift vacancy rates in a single district within a single quarter.

What detailed Malta case studies provide that no general guide can replicate is granular, situated knowledge: how a specific landlord behaved during negotiations, which buildings achieved occupancy fastest after refurbishment, and where fit-out costs exceeded projections. These are the insights that protect budgets and accelerate decision-making. Real-world experience from companies already operating in Malta is, without question, the most reliable input available to any incoming tenant.

Need help finding the right Malta office? See your options

When making a decision that will have an impact on the future of a business, sound advice that can be counted on is crucial. A trusted commercial real estate professional with years of experience will ensure that company objectives are being kept at the forefront of the process.

If you’re ready to apply these lessons to your office search, OfficeSpace.Rent offers the most detailed, current listings across Malta’s key business districts. Explore Mriehel offices to lease for cost-efficient, large floor plate options, or use the full Malta office guide to benchmark requirements across all major locations. For businesses navigating a complex or confidential search, the off-market case study illustrates how we source and secure spaces that never reach the open market.

Frequently asked questions

What is the typical lease length for Malta offices?

Most office leases in Malta run for three to five years, though major anchor tenants can secure significantly longer terms. The Malta Gaming Authority, for example, signed a 15-year SmartCity lease, which is exceptional but illustrates the range available for substantial commitments.

Who pays for office fit-outs in Malta?

In the private sector, the tenant typically bears fit-out costs, though arrangements can vary. Fit-out responsibilities differ for public entities, and landlord contributions are occasionally negotiable for long-term or anchor tenants.

How do office rental prices in Malta compare to other European countries?

Malta offers substantially lower rents than most Western European cities. Sliema averages €250/sqm/yr and Mriehel €170, versus €600 or more in top-tier Dublin or Amsterdam locations.

Which sectors are the leading office tenants in Malta?

iGaming, fintech, aviation, IT, and financial services dominate demand. Tagliaferro Business Centre in Sliema, for instance, houses iGaming, aircraft leasing, IT, and financial services tenants within a single refitted building.

What is the main advantage of renting an office in Malta?

Malta’s primary advantages are English fluency, EU passporting, a concentrated iGaming and fintech ecosystem, flexible lease terms, and rents that are significantly lower than equivalent Western European office markets.