TL;DR:

- Malta’s office market is more sophisticated than its size suggests, with policy reforms expected to boost supply and improve rankings by 2027.

- The market favors tenants seeking smaller spaces due to limited large contiguous floorplates and infrastructure constraints, despite competitive rents and flexible lease terms.

Malta’s office market is considerably more sophisticated than its size suggests, and based on active listings and agency market observations in Q2 2026, the gap between perception and reality is widening. This Malta Office Market Report Q2 2026 covers the metrics that matter most to investors and corporate occupiers: rental rates by district, vacancy dynamics, the policy reforms currently reshaping supply, and where the market is heading through the rest of the year. Malta’s combination of EU membership and English as an official language gives it a structural advantage that competitors in Central and Eastern Europe simply cannot replicate.

Rental ranges and vacancy observations in this report are derived from active market listings, agency discussions, and commercial leasing observations across Malta during Q2 2026. Figures represent indicative asking-rent ranges rather than audited transaction data.

Table of Contents

- Key takeaways

- Supply and demand across Malta’s key districts

- Malta Chamber policy proposals and market impact

- Malta vs. European office hubs: a cost comparison

- Challenges for large-scale occupiers and investors

- Practical leasing and investment considerations for Q2 2026

- My perspective on Malta’s office market

- Find your Malta office space with Officespace

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Prime rents remain competitive | Sliema and St Julian’s command €230 to €450 per sqm annually, far below comparable European capitals. |

| Policy reforms reshaping supply | The Malta Chamber proposed measures including renovation loans and a Derelict Redemption Act to unlock dormant stock. |

| Investment confidence is rising | Recent property transaction indicators suggest continued investment confidence in Malta’s real estate sector. |

| Large floorplate scarcity persists | Contiguous Grade-A space above 1,500 sqm remains limited, constraining very large corporate expansions. |

| Lease flexibility is a genuine advantage | Malta’s standard 2 to 5 year leases offer far more agility than long-term commitments typical in major European cities. |

Supply and demand across Malta’s key districts

The Q2 2026 office market in Malta is best understood district by district, because the dynamics in Mriehel differ substantially from those in Sliema or St Julian’s.

Mriehel, Malta’s recognised CBD, continues to attract the highest concentration of Grade-A office demand. Rents here start at approximately €180 per sqm per year, making it the more affordable choice for occupiers requiring purpose-built, modern stock. Sliema and St Julian’s command a prime rent range of €230 to €450 per sqm annually, reflecting their coastal prestige and proximity to hospitality, retail, and talent pools favoured by iGaming and financial services firms.

| District | Approx. rent (€/sqm/year) | Primary tenant sectors | Grade-A vacancy |

|---|---|---|---|

| Mriehel CBD | €180 to €240 | Finance, tech, corporate HQs | Low to moderate |

| Sliema | €240 to €450 | iGaming, professional services | Low |

| St Julian’s | €250 to €490 | iGaming, fintech, legal | Very low |

| Other localities | €120 to €180 | SMEs, back-office, logistics | Moderate |

Demand remains skewed towards quality. The flight to quality trend observed in major European hubs is playing out in Malta too, with tenants prepared to pay a premium for well-serviced, energy-efficient space. Secondary stock in older buildings continues to soften occupancy, particularly outside the primary coastal and CBD corridors.

Pro Tip: When assessing occupancy data for investment timing, focus on Grade-A vacancy rates rather than blended market figures. A market can show high overall vacancy while Grade-A space remains almost fully let. In Malta, that divergence is currently significant, and it points to a supply deficit at the top end, not a demand problem.

Malta Chamber policy proposals and market impact

The most consequential development shaping Malta’s near-term office space supply is the package of urban policy proposals tabled by the Malta Chamber of Commerce in May 2026.

The proposals target three interconnected problems: empty buildings reducing urban quality, parking congestion deterring office workers, and inconsistent enforcement on construction standards. The Chamber’s Derelict Redemption Act proposal would allow unfinished or derelict buildings to be repurposed through a streamlined regulatory process, directly increasing usable office stock in Urban Conservation Areas where new development is restricted.

The likely market impacts include:

- Renovation loan access: Interest-free renovation loans targeted at Urban Conservation Area properties would lower the financial barrier for landlords to upgrade older Grade-B stock, potentially shifting a portion into higher-yield, leasable Grade-A condition.

- Parking fee reform: Fees collected from urban parking would transfer to e-mobility wallets rather than general revenue, incentivising alternative commute methods and reducing congestion around dense office clusters.

- Construction enforcement: Tighter penalties on abandoned or unfinished structures would reduce blight, which indirectly affects tenant perceptions of the areas surrounding their office addresses.

- Dormant stock activation: The Derelict Redemption Act creates a legal pathway for bringing buildings that have sat unused for years back into productive commercial use.

If implemented, these measures would meaningfully shift the supply picture for the 2027 to 2028 period. For investors watching the Malta property market outlook, the renovation loan scheme is particularly relevant: assets in established urban areas that currently trade at a discount to Grade-A rents could become strong repositioning opportunities.

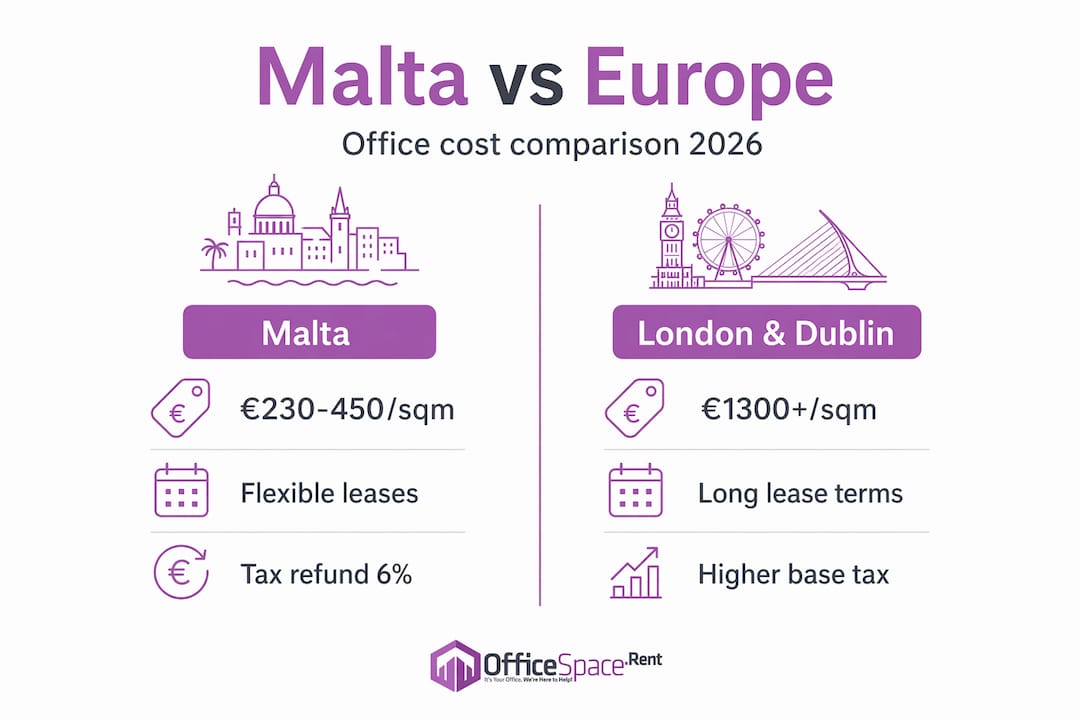

Malta vs. European office hubs: a cost comparison

Malta’s cost position relative to major European office markets is one of the least-appreciated factors in corporate real estate planning. Prime London rents run approximately 5 to 6 times higher than Malta’s top-end rates, and even Lisbon and Dublin now command significantly higher per-sqm costs following sustained demand growth over the past decade.

| City | Prime rent range (€/sqm/year) | Typical lease term | English-language environment |

|---|---|---|---|

| Malta (Sliema/St Julian’s) | €230 to €450 | 2 to 5 years | ✅ Official language |

| Lisbon | €240 to €330 | 5 to 10 years | Partial |

| Dublin | €400 to €600 | 5 to 15 years | ✅ |

| London (City) | €1,100 to €1,500 | 5 to 25 years | ✅ |

The rent differential is significant, but the lease flexibility advantage is equally important for growing businesses. Malta’s 2 to 5 year lease norms allow companies to scale their footprint without being locked into decade-long commitments that restrict agility. For a Series B technology company or a regulated financial services firm establishing a European base, that flexibility has real option value.

The fiscal dimension adds another layer. Malta’s corporate tax refund system can reduce the effective tax rate to approximately 5% for qualifying businesses, well below the headline 35% rate. When combined with office rental costs that are a fraction of Dublin or London equivalents, the total cost of a Malta base can be substantially lower than many boards initially model.

Pro Tip: If you are modelling a European headquarters decision, do not calculate office cost in isolation. Factor in corporate tax treatment, payroll costs, and lease term flexibility together. Malta’s combined position often looks materially stronger than a headline rent comparison suggests.

Challenges for large-scale occupiers and investors

A balanced Q2 2026 office market analysis requires acknowledging where Malta’s structural limitations create genuine constraints.

- Large contiguous floorplates are scarce. Grade-A space above 1,500 sqm in a single contiguous block is limited. Organisations requiring 2,000 sqm or more under one roof face a constrained shortlist and must accept longer lead times or consider design-and-build solutions.

- Road infrastructure limits logistics efficiency. Malta’s road network is well known for congestion, which matters for businesses with operationally sensitive commute or client access requirements. This affects site selection within the island and should be weighted when comparing Mriehel against coastal options.

- Workforce scalability has a ceiling. Malta’s total population of approximately 550,000 means that very rapid headcount growth of 200 or more specialist hires within 12 months is challenging. Businesses that may need to hire aggressively should plan talent pipelines early, often before signing a lease.

- Developer pipeline is thin for new large schemes. Unlike Dublin or Warsaw, Malta has no significant speculative Grade-A development pipeline of the scale that could satisfy a 5,000 sqm requirement within a short timeframe.

Understanding these constraints upfront prevents expensive misalignment between corporate property strategy and what the Malta market can realistically deliver. For companies whose requirements sit below the 1,500 sqm threshold, these limitations are far less material.

Practical leasing and investment considerations for Q2 2026

Translating the data above into decisions requires a structured approach. These are the most relevant factors for investors and occupiers acting on Q2 2026 market conditions:

- Assess building quality against the policy window. The interest-free renovation loans proposed by the Chamber create a limited-time opportunity for investors to acquire underperforming assets in Urban Conservation Areas and reposition them ahead of a likely uplift in tenant quality expectations. Investors wanting to understand the financing side of such repositioning can explore options like a bridge loan to cover acquisition-to-renovation gaps.

- Time your entry with the supply cycle. Grade-A vacancy is currently low, giving landlords pricing power. Tenants who can act now before further policy-driven supply restriction tighten availability will secure better terms.

- Select location based on your talent profile. iGaming and fintech businesses consistently favour St Julian’s and Sliema for proximity to lifestyle amenities that attract young international professionals. Finance and corporate services often prioritise Mriehel for its modern stock and central island position.

- Negotiate lease terms actively. Malta’s market supports tenant-favourable negotiations on fit-out contributions and break clauses, particularly in secondary stock where landlords face longer void periods.

For a detailed breakdown of Malta office locations, including district-level data and accessibility assessments, Officespace provides dedicated resources built specifically for corporate decision-makers.

My perspective on Malta’s office market

In my experience watching this market since 2015, the most persistent mistake investors make is underestimating Malta because of its size. The island consistently punches above its weight as a European business location, and the policy agenda now being proposed is the most coherent attempt yet to address the supply-side weaknesses that have held the market back.

The urban regeneration push matters. Bringing dormant stock into productive use, combined with fiscal incentives for property upgrades, could quietly add meaningful Grade-B-to-A conversion volume over the next two to three years. That is not reflected in current pricing, which means early movers stand to benefit.

I would caution, however, against over-positioning Malta as a large-occupier solution. The physical constraints on floorplate size are real, and no amount of policy reform changes the geography. Where Malta genuinely wins is for sub-1,500 sqm requirements where cost savings, lease flexibility, and English-language advantage combine to create a compelling total value proposition that very few European locations can match at equivalent quality.

— OfficeSpace.Rent

Find your Malta office space with Officespace

Officespace has been Malta’s specialist commercial property platform since 2015, and the Q2 2026 market conditions described in this report are reflected in real-time across our listings database. Whether you are an investor seeking commercial property for sale across Malta or a corporate tenant evaluating options in Mriehel, Sliema, or St Julian’s, our platform provides filtered search, verified pricing data, and direct agent access. You can also explore prominent commercial premises for sale if you are seeking high-visibility assets with strong investment fundamentals. Our team supports the full leasing cycle, from initial search through to lease execution.

FAQ on Malta Office Market Report Q2 2026

What are current prime office rents in Malta?

Prime office rents in Sliema and St Julian’s range between €230 and €450 per sqm per year in 2026, with Mriehel CBD offering lower-cost Grade-A options from approximately €180 per sqm annually.

How does Malta’s office market compare with London or Dublin?

Malta’s prime rents run approximately 5 to 6 times lower than central London, and are also significantly below Dublin, while offering English as an official language and shorter, more flexible lease terms.

What is the Derelict Redemption Act proposed in 2026?

The Derelict Redemption Act is a Malta Chamber of Commerce proposal from May 2026 designed to allow unfinished or abandoned buildings to be repurposed through a simplified regulatory process, increasing available commercial stock in Urban Conservation Areas.

What are the main challenges for large occupiers in Malta?

The primary constraint is a limited supply of contiguous Grade-A floorplates above 1,500 sqm, alongside road congestion and a finite local workforce, which can restrict rapid large-scale expansion on the island.

Is Malta a good location for a European business base in 2026?

For organisations requiring under 1,500 sqm, Malta offers a strong combination of competitive rents, lease flexibility, a corporate tax system with effective rates potentially as low as 5%, and high English fluency across the workforce, making it a credible and cost-effective European base.

Recommended

- Malta Office Market Pricing Trends for 2026 – Offices in Malta To Let & For Sale

- About Office Space.Rent – Malta’s Office Specialists Since 2015

- Malta Office Locations: A Comprehensive Guide – Offices in Malta To Let & For Sale

- Sliema Office Market Update on Current Trends – Offices in Malta To Let & For Sale