TL;DR:

- Certain qualifying rental income may be eligible for an optional 15% final withholding tax regime under Maltese tax legislation. Most companies conducting business operations remain subject to the standard corporate income tax system.

- Classifying rental income as passive or trading significantly impacts deductibility, VAT obligations, and overall tax treatment.

Tax implications for office rentals in Malta are determined by two factors: the tax regime a business selects and whether the rental income is classified as passive or active trading income. Certain qualifying rental income may be eligible for an optional 15% final withholding tax regime under Maltese tax legislation. Most companies conducting business operations remain subject to the standard corporate income tax system. The 2026 Budget introduced significant new incentives, including a 175% deduction for research, development, and innovation expenditure, which directly affects how businesses should structure their office leasing costs. Getting this classification right from the outset is the difference between a tax-efficient operation and an avoidable liability.

What are the main tax regimes for office rental income in Malta?

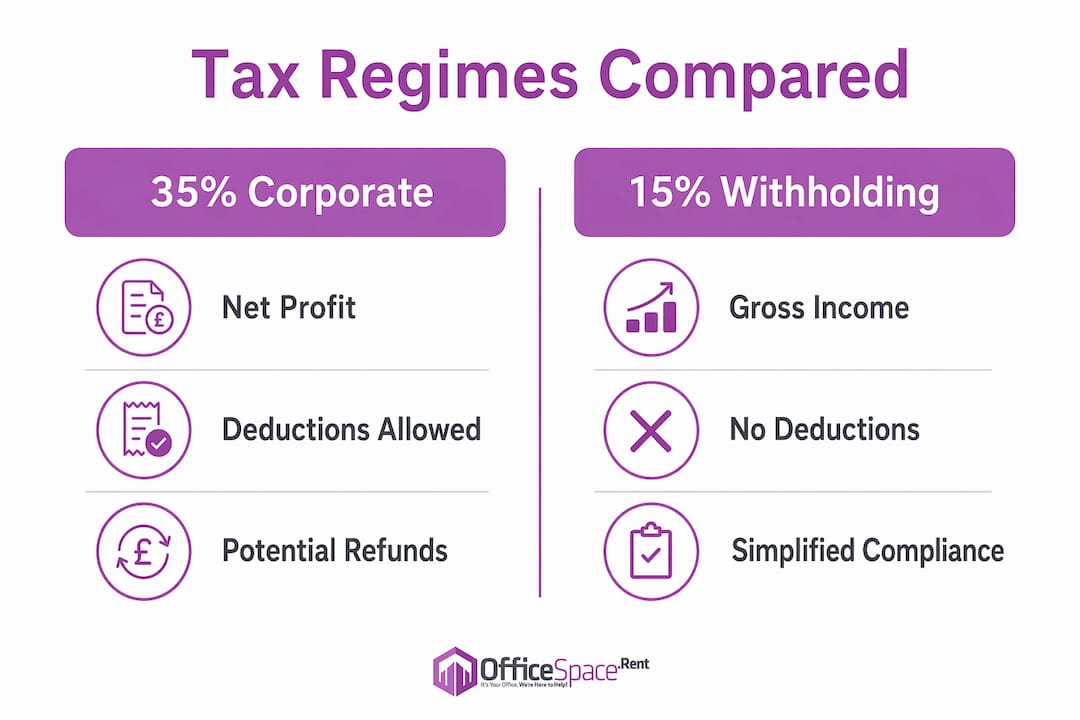

Malta gives businesses a clear binary choice when it comes to taxing office rental income. The standard corporate tax regime applies at 35% on net profit, but companies can claim deductions for allowable expenses and benefit from Malta’s shareholder refund mechanism, which can reduce the effective rate substantially. The 15% final withholding tax applies to gross rental income with no deductions permitted and no refund available.

The table below compares the two regimes directly.

| Feature | 35% corporate tax | 15% final withholding tax |

|---|---|---|

| Tax base | Net profit after deductions | Gross rental income |

| Deductions allowed | Yes | No |

| Shareholder refund | Eligible | Not eligible |

| Compliance complexity | Higher | Lower |

| Best suited for | Businesses with significant deductible expenses | Businesses with minimal deductible costs |

Choosing the 15% regime simplifies compliance by removing the need to track and document deductions. However, it will be less tax-efficient for businesses carrying substantial operational costs such as agency fees, utilities, service charges, and fit-out expenditure. The decision between the two regimes should be made after modelling actual deductible expenses — not chosen for administrative convenience alone.

Pro Tip: If your annual office rental expenses exceed roughly one third of your gross rental income, the 35% corporate tax regime with deductions will almost always produce a lower effective tax burden than the 15% flat rate. Run both calculations with your tax adviser before filing.

How does Malta classify office rental income: passive vs. trading?

The distinction between passive and trading income is the most consequential classification decision in Maltese office rental taxation. It determines which expenses you can deduct, how losses are treated, and whether VAT and licensing obligations apply.

Passive rental income arises from long-term letting of office space without additional services. Key characteristics include:

- Deductions are limited to expenses directly incurred against the passive income.

- Losses from passive rental activity can only be set off against other passive profits, not against trading income.

- The income is reported under the corporate tax return as investment income.

Trading income arises when the rental activity constitutes a commercial operation. This typically applies to businesses operating serviced offices, short-term lettings, or multiple units with active management. The implications are materially different:

- A broader range of expenses becomes deductible, including staff costs, management fees, and service charge contributions.

- Losses can be offset against other trading income streams.

- VAT registration and licensing obligations apply, adding compliance requirements.

- The activity is treated as a trade, which affects how refunds are calculated under the corporate tax system.

Misclassifying trading activity as passive income is a common error in Malta. It can result in disallowed deductions and penalties from the Commissioner for Tax and Customs. Businesses operating more than one office unit or providing ancillary services alongside their letting activity should seek a formal classification opinion from a Maltese tax adviser before filing.

What expenses are deductible and how do 2026 incentives apply?

Allowable operational expenses under the 35% corporate tax regime include rent paid on sub-leased premises, interest on borrowings used to finance the office, utilities, service charges where passed through to the business, and agency fees. These costs reduce the taxable base and directly lower the corporate tax liability before any refund mechanism applies.

The 2026 Budget introduced two significant incentives that interact directly with office rental expenditure. First, a 175% RDI tax deduction is available on qualifying research, development, and innovation expenditure. Capital investments already eligible for standard capital allowances are excluded from this deduction to prevent double claims. Capital expenditure is spread over six years under the standard allowance rules.

Second, businesses investing in office modernisation — including structural upgrades and digital infrastructure — can access tax credits of up to 60% of qualifying expenditure under 2026 legislation. That credit represents a direct reduction in tax liability, not merely a deduction from taxable income. The distinction matters significantly for cash flow planning and lease negotiation strategy.

Pro Tip: Align office fit-out and equipment purchases with the capital allowance schedule before claiming the RDI deduction. Claiming both on the same asset triggers a disallowance. Document each expenditure category separately from the outset and confirm eligibility with your tax adviser before works are commissioned.

The 2026 tax strategy effectively converts ordinary office rental and fit-out costs into qualifying capital investments, provided businesses maintain thorough documentation and align expenditure approvals with the requirements of the Maltese tax authority. This is not automatic. It requires deliberate planning before lease contracts are signed and fit-out contracts are placed.

How do substance requirements affect tax treatment of office rentals in Malta?

Malta’s favourable effective tax rates are conditional on genuine economic substance. Substance requirements mandate that companies maintain physical premises, employ local staff, and incur proportional operational expenses. Without this, the tax benefits do not apply regardless of the structure adopted.

The consequences of failing substance tests are severe:

- Participation exemptions are denied, removing a key mechanism for reducing tax on dividends and capital gains.

- Treaty benefits under Malta’s double tax agreement network become unavailable.

- Rental income may be reclassified, attracting higher taxation.

- Refund claims under the 35% corporate tax regime can be rejected.

To qualify for Malta’s reduced effective tax rate, office lease activity must be supported by documented local staff presence, proportional operational expenditure, and genuine business risk-taking at the Maltese entity level. A registered address alone does not satisfy this requirement.

Robust record-keeping is the practical foundation of substance compliance. Businesses should maintain board minutes showing decisions taken in Malta, signed lease agreements, payroll records for local employees, and evidence of operational expenditure. Tax advisers consistently warn against using Maltese companies as passive investment vehicles without genuine substance, as this triggers higher tax rates and forfeiture of treaty benefits. The office rental process guide for financial firms outlines how to structure lease agreements to support these requirements from day one.

Key takeaways

Malta’s tax treatment of office rental income depends on regime selection and income classification, making early planning the most effective cost-reduction tool available to business owners.

| Point | Details |

|---|---|

| Regime selection matters | The 35% corporate tax with deductions suits expense-heavy businesses; the 15% flat rate suits those with minimal deductible costs. |

| Classification drives deductibility | Trading income allows broader deductions and loss offsets; passive income has strict limits on both. |

| 2026 incentives reward investment | A 175% RDI deduction and up to 60% tax credits apply to qualifying office modernisation expenditure. |

| Substance is non-negotiable | Physical premises, local staff, and documented expenditure are prerequisites for favourable tax rates and treaty benefits. |

| Documentation prevents disputes | Board minutes, lease contracts, and payroll records protect refund claims and treaty eligibility against challenge. |

Officespace’s view on tax-efficient office leasing in Malta

Having worked closely with businesses establishing operations in Malta, the pattern is consistent: the companies that extract the most value from Malta’s tax framework are those that treat the office lease decision as a tax planning decision, not just a property decision.

The most common mistake is selecting the 15% final withholding tax regime for its simplicity without first calculating whether deductible expenses would make the 35% system more efficient. The second most common mistake is failing to document substance from the first day of trading. By the time a tax authority query arrives, reconstructing historical records is costly and rarely convincing.

The 2026 RDI incentives represent a genuine opportunity to reclassify office modernisation costs as qualifying capital investment. Most businesses are not taking advantage of this because they are not coordinating their property and tax advisers before signing leases or commissioning fit-out works. A fit-out that qualifies for a 60% tax credit is not an expense. It is a funded investment. That framing changes how businesses should approach lease negotiations and rental cost structures entirely.

The businesses that get this right share one trait: they sign the lease after the tax plan, not before it.

— Officespace

How Officespace supports tax-efficient office rentals in Malta

Officespace lists commercial office spaces across Malta’s key business districts, including offices in Attard and commercial premises in Birkirkara, both of which are locations frequently used by businesses establishing genuine economic substance for tax purposes. Every listing includes detailed information on size, lease terms, and pricing to support informed decisions before contracts are signed.

Beyond listings, Officespace provides lease negotiation support and guidance on structuring rental agreements to align with Malta’s substance requirements and deductibility rules. For businesses planning to claim office modernisation tax credits under 2026 legislation, selecting the right premises and lease structure from the outset is critical. Officespace’s local market expertise helps businesses connect property decisions with tax planning objectives from day one.

FAQ

What is the tax rate on office rental income in Malta?

Malta offers two options: a 35% corporate tax on net profit with deductions and potential shareholder refunds, or a 15% final withholding tax on gross rental income with no deductions permitted and no refund available. The right choice depends on the level of deductible expenses the business carries.

Can I deduct office rental expenses from my Maltese tax bill?

Deductions are permitted under the 35% corporate tax regime and include rent, utilities, service charges, interest on borrowings, and agency fees. The 15% final withholding tax disallows all deductions. Where deductible expenses are material, the 35% regime will typically produce a lower effective tax burden.

What is the 175% RDI deduction introduced in the 2026 Budget?

The 175% RDI deduction applies to qualifying research, development, and innovation expenditure under Maltese 2026 budget legislation. Capital investments already claimed under standard capital allowances are excluded to prevent double claims. Businesses should document each expenditure category separately and confirm eligibility with their tax adviser before committing expenditure.

How do substance requirements affect my office rental tax benefits in Malta?

Failing to demonstrate genuine substance — including a physical office, local staff, and proportional operational expenditure — risks denial of participation exemptions, treaty benefits, and corporate tax refunds under Maltese law. A registered address without operational activity does not satisfy the requirement.

Does passive rental income qualify for Malta’s low effective tax rate?

Passive rental income can benefit from the 35% corporate tax system with shareholder refunds, but only if the business demonstrates genuine economic substance. A registered address without documented local staff presence, board activity in Malta, and proportional operational expenditure does not qualify.